Blog

We keep you up to date on the latest tax changes and news in the industry.

Big Changes for Vehicle Tax Deductions

Article Highlights:

- Standard Mileage Rates

- Actual Expense Method

- Vehicle Depreciation

- Vehicle Interest Expenses

- Sale or Trade-in of a Business Vehicle

- Employees

Standard Mileage Rates – The standard mileage rates for the business use of a car (or a van, pickup, or panel truck) are:

|

STANDARD MILEAGE RATES FOR BUSINESS

|

|

|

2017

|

2018

|

|

53.5 Cents Per Mile

|

54.5 Cents Per Mile

|

However, the standard mileage rates cannot be used if you have used the actual expense method (using Sec. 179, bonus depreciation and/or MACRS depreciation) in previous years. This rule is applied on a vehicle-by-vehicle basis. In addition, the business standard mileage rate cannot be used for any vehicle used for hire or for more than four vehicles simultaneously.

Actual Expense Method - Taxpayers always have the option of calculating the actual costs of using their vehicle for business rather than using the standard mileage rates. In addition to the potential for higher fuel prices, the extension and expansion of the bonus depreciation, as well as increased depreciation limitations for passenger autos in the Tax Cuts and Jobs Act, may make using the actual expense method worthwhile during the first year a vehicle is placed in business service. Actual expenses include:

- Gasoline

- Oil

- Lubrication

- Repairs

- Vehicle registration fees

- Insurance

- Depreciation (or lease payments).

Vehicle Depreciation - The so-called “luxury auto” rules limit the annual deduction for depreciation. Tax reform substantially increased these limits providing much larger first and second-year deductions for more expensive vehicles. The table below displays the limits that apply to vehicles placed in service in 2017 and 2018 and shows the substantial increase for 2018. These rates are inflation adjusted in subsequent years.

Tax reform also included 100% bonus depreciation, which, at the election of the taxpayer, can be added to the first-year luxury auto rates (see the amounts for “First Year with Bonus” in the table below). However, instead of an $8,000 increase, if the vehicle was purchased before September 28, 2017, but not put into service until 2018 or 2019, the increase to the first year depreciation cap is only $6,400 or $4,800, respectively, rather than $8,000.

|

LUXURY AUTO DEPRECIATION LIMITS

|

||||

|

Trucks & Vans

|

Automobiles

|

|||

|

2017

|

2018

|

2017

|

2018

|

|

| First Year |

3,560

|

10,000

|

3,160

|

10,000

|

| First Year with Bonus |

11,560

|

18,000

|

11,160

|

18,000

|

| Second Year |

5,700

|

16,000

|

5,100

|

16,000

|

| Third Year |

3,450

|

9,600

|

3,050

|

9,600

|

| Thereafter |

2,075

|

5,760

|

1,875

|

5,760

|

Vehicle Interest Expenses - Regardless of whether the standard mileage rate or actual expense method is used, a self-employed taxpayer may also deduct the business use portion of interest paid on an auto loan on their Schedule C. However, employees may not deduct interest paid on a consumer car loan.

Sale or Trade-in of a Business Vehicle – Under prior law, it was good tax strategy to trade-in a vehicle that would result in a gain, thus deferring the gain into the replacement vehicle and avoiding the tax on the gain. On the other hand, it was good practice to sell a vehicle for a loss and take advantage of the tax loss. Unfortunately tax reform no longer allows tax-deferred exchanges for anything but real estate. This does away with the aforementioned strategies, and now all sales and trade-ins are treated as sales, with any gain being taxable and any loss being deductible. However, a loss on the sale of a vehicle used solely for personal purposes is not deductible, and if the vehicle was used both for business and personal reasons, only the business portion of the loss is deductible.

Employees – Tax reform also eliminates the itemized deduction for employee business expenses; this is the place on the tax return where employees could deduct the business use of their vehicle for their employer. Thus, business vehicle expenses are no longer deductible by employees.

Please call if you have questions related to the business use of your vehicle.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

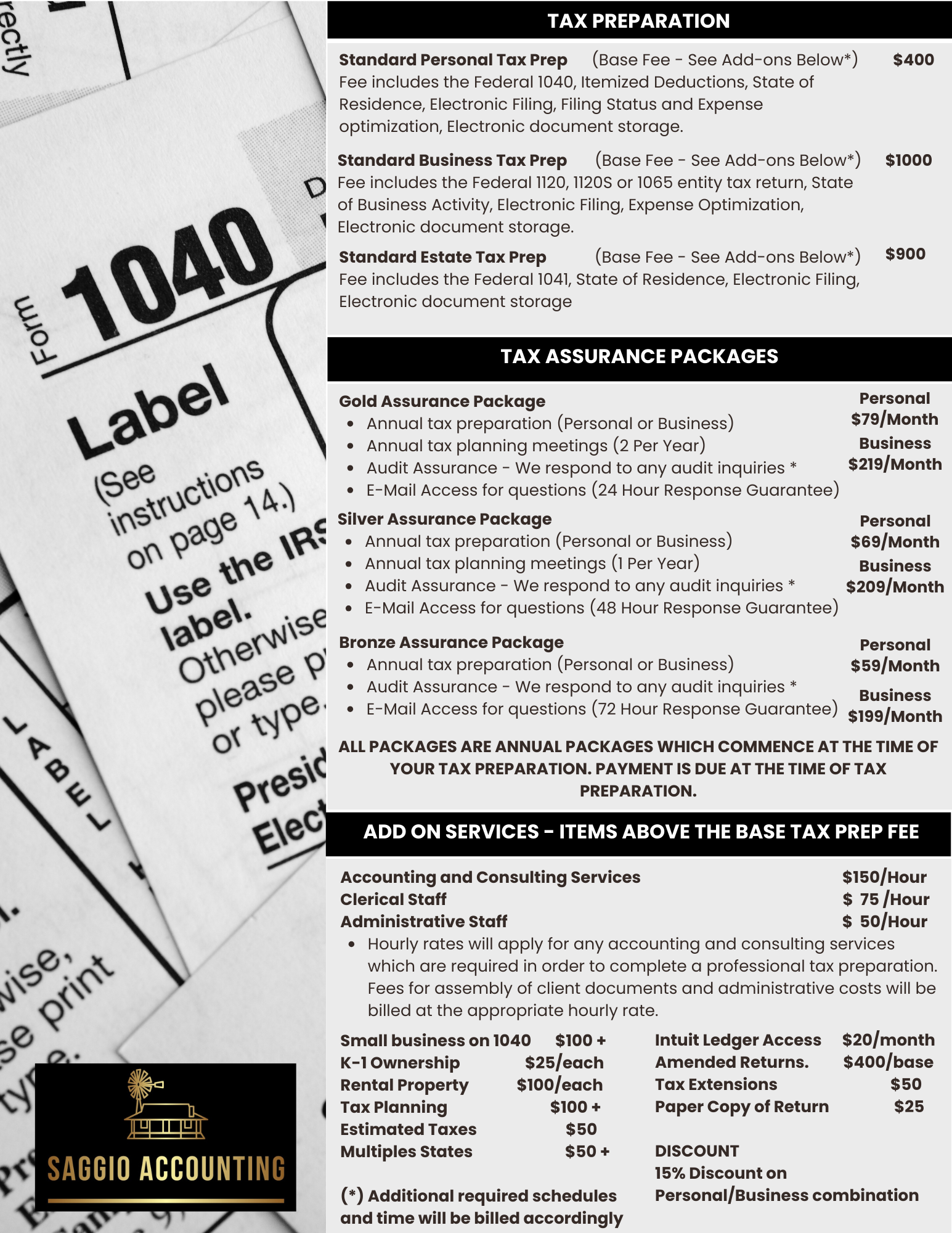

TAX ASSURANCE PRICING

Personal Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages.

Bronze Assurance Package

-

Annual Tax Preparation

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail Access for questions (36 Hour Response)

TAX ASSURANCE PRICING

Business Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages. These packages include both the business and personal tax related preparation services.

Bronze Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail access for questions (48 Hour Response)