Blog

We keep you up to date on the latest tax changes and news in the industry.

Haven't Filed Tax Returns for Multiple Years? Here's What You Need to Do Next

You'd be hard-pressed to find someone who actually enjoys the process of filing taxes. Having said that, it's absolutely something that you're supposed to do like clockwork every single year.

Of course, there are a myriad of different reasons why you may have fallen behind. You could be going through something of a major life transition and simply were unable to meet the filing deadline. Maybe you filed for a much-needed extension and then other things got in the way (as they often do), causing you to fall behind even further.

Regardless of the reason, it's important to take meaningful steps to get yourself back on track before it's too late. Thankfully, this isn't necessarily a difficult process - but it will require you to keep a number of important things in mind along the way.

The Consequences of Not Filing Your Taxes for Multiple Years

But first, it's important to understand the actual consequences of what can happen if you don't file your taxes for multiple years in a row - or even for ten years or more in some situations.

The most immediate impact you're likely to experience will come by way of the IRS itself. If you have income that you haven't reported on your taxes, you will be charged various penalties and fees on everything that you should have been paying up until now. These can and often do quickly add up to significant sums of money, which is why it is always important to get on track as soon as you're able to.

Keep in mind that the IRS will charge you those fees and penalties on all taxable income, not taking into consideration any credits or deductions that you would have enjoyed had you filed taxes on time. They don't have records pertaining to expenses like your rent or other things that you need for your job like essential equipment. Because of this, any fees will be assessed based on what they think you owe - not necessarily on what you actually owe.

If it is determined that you have been "willfully" failing to file taxes, you could potentially be punished with up to five years in prison. Likewise, you could get hit with a fine of up to $100,000 if your situation is considered to be "tax evasion." Needless to say, these are all consequences that you would do well to avoid at all costs.

There are other consequences involved with not filing your taxes for a lengthy period of time, too. Sometimes when you file for a passport, for just one example, you may be asked to show your recent tax returns as a form of income verification. Obviously, you can't do that if you haven't been filing them. The same is true if you were planning on applying for a mortgage or car loan.

If retirement is coming up, it could also impact the types of benefits that you will receive like Social Security and Medicare. All of these are crucial aspects of life that you do not want to jeopardize, so you should get your taxes taken care of sooner rather than later.

Getting on Track With Your Taxes: A Plan of Action

The first thing you should do to get back on track with your taxes involves checking on the current status of your account with the IRS. At the very least, this will give you an indication of what the IRS thinks you owe. You can do so at the official website via irs.gov, or by calling 1-800-829-1040 to speak to a live representative.

At that point, you have two options available to you. The first involves paying what the IRS currently says you owe, along with both the original taxes and any fees or penalties that have accrued, to settle your account. If you can't pay the full balance in one lump sum, you could always attempt to get on a payment plan.

The second involves gathering all the financial information you need to complete the tax forms you did not file. You'll need to compile several important documents, including but not limited to things like:

Any information pertaining to the income you made during the missing years, along with any expenses that you had so that you can claim deductions and credits that apply to you.

Any supporting documentation like receipts and income statements that are necessary to complete the aforementioned financial records. This may require you to perform some forensic accounting so that you have the most complete picture to work from.

At that point, the next step is clear: you should file your missing tax returns at your earliest convenience. Thankfully, there is no time limit associated with filing those old tax returns. However, the sooner you do it, the better.

Oftentimes, this is absolutely the way to go as once all documents and other financial information have been properly recorded, you'll likely end up owing less than the IRS thinks you do. You'll still owe money, but you'll save a bit in the long run.

Finally, you should pay your taxes as soon as you can. Again, you can do this either through a lump sum or get on some type of payment plan to bring your account up-to-date. You may also choose to look into a settlement agreement or any type of income tax forgiveness that may apply to you. You could even choose to make what is known as an "offer in compromise," which allows you to pay something towards your balance to consider everything settled. The IRS would have to agree with whatever offer you make, of course.

At that point, you should prepare for future taxes so that you don't find yourself in the same position down the road. If you need help doing precisely that, or if you have any additional questions about this process that you'd like to see answered, please don't delay - contact us to speak to a tax professional today.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

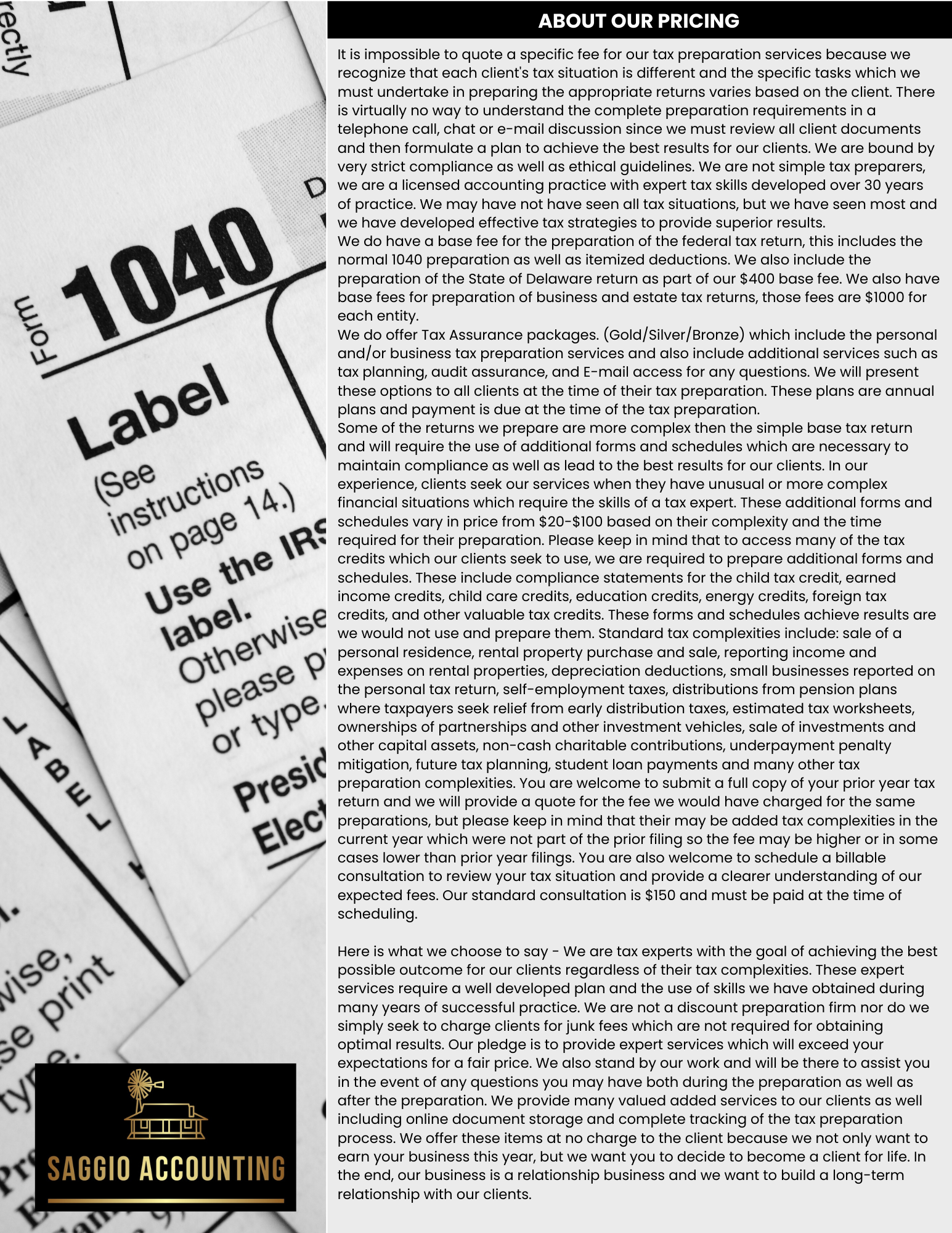

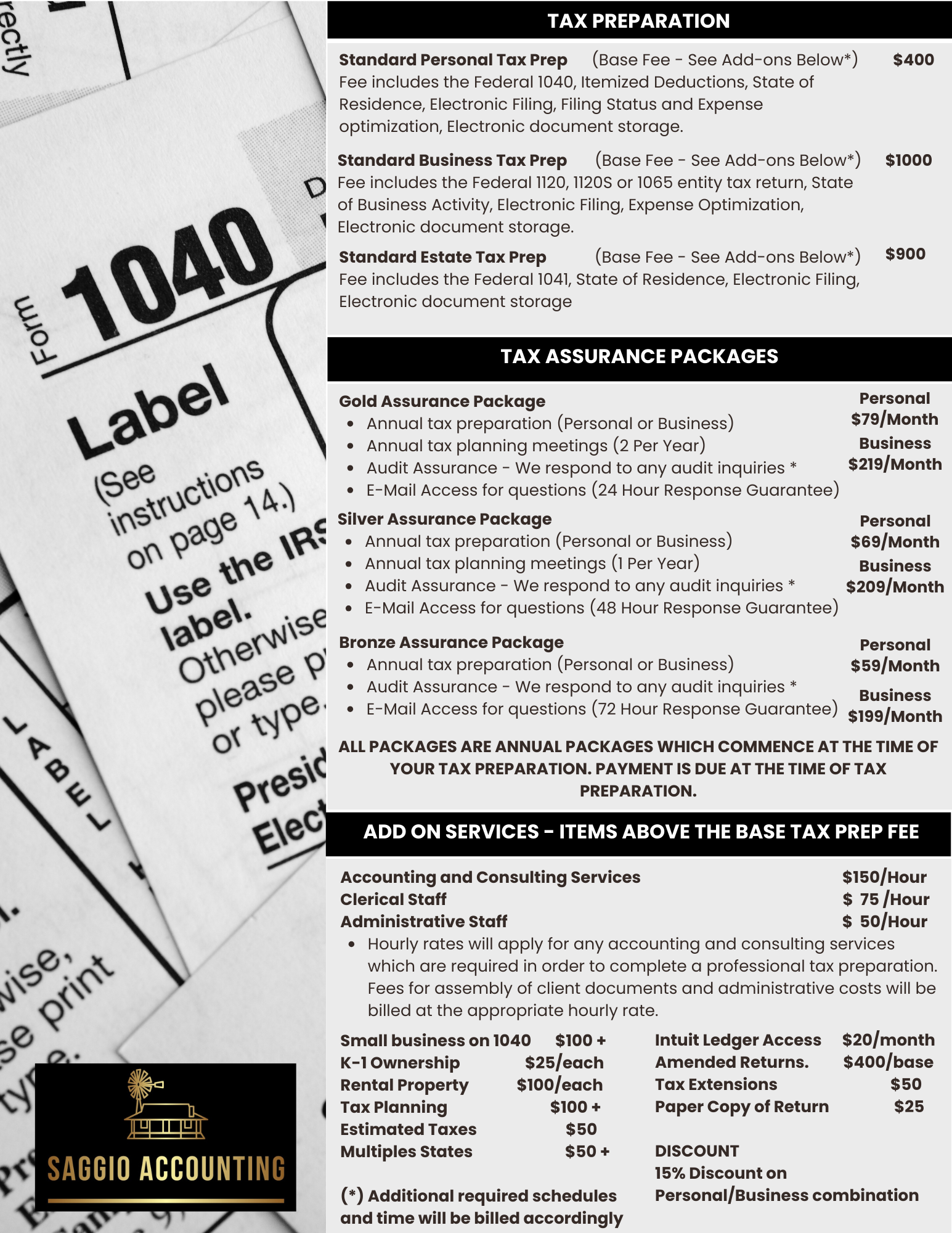

TAX ASSURANCE PRICING

Personal Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages.

Bronze Assurance Package

-

Annual Tax Preparation

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail Access for questions (36 Hour Response)

TAX ASSURANCE PRICING

Business Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages. These packages include both the business and personal tax related preparation services.

Bronze Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail access for questions (48 Hour Response)