Blog

We keep you up to date on the latest tax changes and news in the industry.

Here’s How To Take A Page From The Ultra-wealthy Playbook And Make Full Use Of Roth Individual Retirement Accounts

We’ve all heard the term “the rich get richer.” According to a report released from ProPublica, it turns out that one of the ways that truism is perpetuated is through the strategic use of tax-sheltered Roth individual retirement accounts (IRAs). The good news is that the same approach is available to the man on the street. The only thing you need is the know-how.

How the ultra-wealthy use Roth IRAs

The story details how ultra-smart people have become ultra-wealthy, accumulating millions and billions of dollars through the Roth’s tax sheltering properties. Where these accounts don’t offer the upfront tax break that you get with traditional 401(k) plans and IRAs, they are tax-advantaged when it comes time to make withdrawals. And the same investors who are blocked from contributing directly to a Roth due to their higher income have the option of converting assets that are held in a traditional IRA or 401(k) into a Roth. Though they still need to pay taxes on the money that they roll into the new account, once it’s there it can be withdrawn with no tax impact after it’s been held a minimum of five years and the account holder reaches the age of 59 1/2, or it can be kept in the account where it grows tax free.

The ProPublica report explains that this strategy grew an account valued at under $2,000 in 1999 to one worth $5 billion for Paypal founder Peter Thiel, who sheltered his investments in what is known as a self-directed Roth IRA, which offers identical tax advantages of untaxed distributions and growth as a standard Roth IRA, while at the same time providing more investment opportunities such as shares in private companies or in real estate. That’s how Thiel grew his account, holding shares of PayPal long before it became a publicly traded company.

As attractive as self-directed IRAs sound, there are some caveats. You are not going to be able to invest in them through traditional firms like Vanguard or Fidelity Investments. Instead, you’ll need to contact a specialized custodian who can facilitate your purchase but will not provide you with any advice on your investments, including telling you if what you’re doing is legal or not. Choosing to get involved in a self-directed IRA is a decision to go it alone and accept the consequences. You need to do your homework, both on what is allowed and isn’t and on the value of the alternative assets you choose. It may seem like an insignificant detail, but not paying attention to it puts you at risk for breaking tax laws.

All the cautionary notes aside, investing in assets within a self-directed IRA gives you the advantages of the tax-free Roth products and allows you to sell what you’re holding at a profit and then roll those gains into new asset purchases within the same account. Alternatively, you can go the more traditional route and select the standard Roth IRA and invest in high growth potential investment options. Doing so helps bypass worries about liquidating traditional IRA or 401(k) holdings after retirement and risking higher future tax rates, as well as having to meet the Required Minimum Distribution amounts that those accounts impose on you if you are the original account owner and you reach the age of 72.

If you have questions about tax-advantaged retirement savings options, contact our office.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

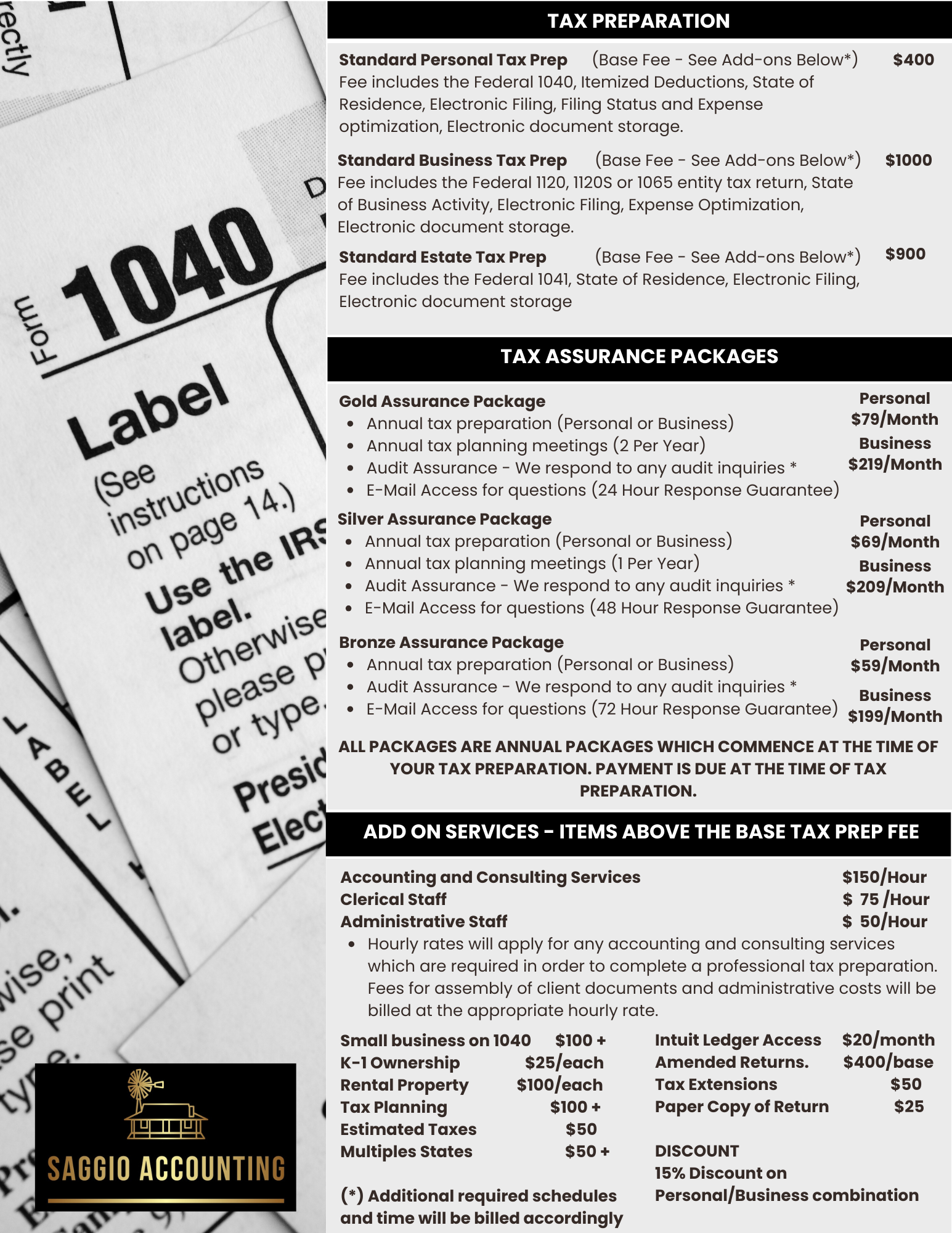

TAX ASSURANCE PRICING

Personal Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages.

Bronze Assurance Package

-

Annual Tax Preparation

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail Access for questions (36 Hour Response)

TAX ASSURANCE PRICING

Business Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages. These packages include both the business and personal tax related preparation services.

Bronze Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail access for questions (48 Hour Response)