Blog

We keep you up to date on the latest tax changes and news in the industry.

The Obscure Research Credit

Article Highlights:

·

Credit

Purpose

·

Credit

Amount

·

Simplified

Credit Calculation

·

Failure

to Take Advantage of the Credit

·

Small

Business Features

·

Qualified

Research Expenses

·

Business

Qualifications

An obscure tax credit—generally referred to as the R&D (research and development) credit—was originally added to the tax code in 1981 as a two-year incentive for businesses and has been extended every year since, until it was recently made permanent.

The purpose of the credit is an inducement and reward to get U.S. companies to increase their investment in research and development for new, improved, or technologically advanced products or trade processes, thus keeping the U.S. competitive with the rest of the world. Other applications of the credit may include improvement upon the functionality, reliability, performance, or quality of existing products or trade processes.

The credit (IRC Sec 41) is generally 20% of the increase in research activities over a base amount and includes some very complicated calculations related to payments made to certain outside organizations and for energy research.

The base amount is a fixed percentage of a taxpayer’s average annual gross receipts from a U.S. trade or business, net of returns, and allowances for the 4 tax years before the credit year. It can’t be less than 50% of the current year’s qualified research expenses.

There is also a simplified credit calculation, which may be more suitable for a smaller business, that is equal to 14% (instead of 20%) of the excess of the qualified research expenses for the tax year over 50% of the average qualified research expenses for the three tax years preceding the tax year for which the credit is determined.

Most of the complications involve larger businesses, while smaller businesses may fail to take advantage of the credit, not realizing those complications probably do not apply to them. Thus, many medium- to small-size businesses fail to claim the credit. The good news is that if your company qualifies for the credit and hasn’t utilized it, it can be claimed on an amended tax return for a prior year that is within the statute of limitations.

The credit also includes two features that are favorable to small businesses ($50 million or less in gross receipts).

· They may claim the credit against the alternative minimum tax (AMT) liability, and

· The credit can be used by even smaller businesses ($5 million or less in gross receipts) against the employer’s part of the Social Security portion of the employer’s payroll tax (the FICA liability).

To qualify for the credit, the research and development must be conducted on U.S. soil (including Puerto Rico and U.S. possessions) and generally includes qualified research expenses, defined by the tax code as:

· Qualified wages paid to or incurred by an employee.

· Supplies used in research and development other than:

o Land and improvements to land and

o Property that is subject to depreciation.

· Contract research expenses paid to a person other than an employee for qualified research. However, only 65% of these expenses qualify.

· Consortium expenses (research expenses paid to certain nonprofits engaged in scientific research) limited to 75% of the expense.

· Amounts paid to eligible small businesses, universities, and federal laboratories.

· Qualified energy research at 100% of the expense.

To qualify for the credit, the taxpayer must show that the activities:

· Are intended to resolve technological uncertainty related to the capability or methodology for developing or improving the business component or the appropriate design of the business component.

· Rely on a hard science, such as engineering, computer, biological, or physical science.

· Are related to the development of a new or improved business component, defined as new or improved products, processes, internal use computer software, techniques, formulas, or inventions to be sold or used in the taxpayer’s trade or business, and

· Entirely constitute a process of experimentation involving testing and evaluation of alternatives to eliminate technological uncertainty.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

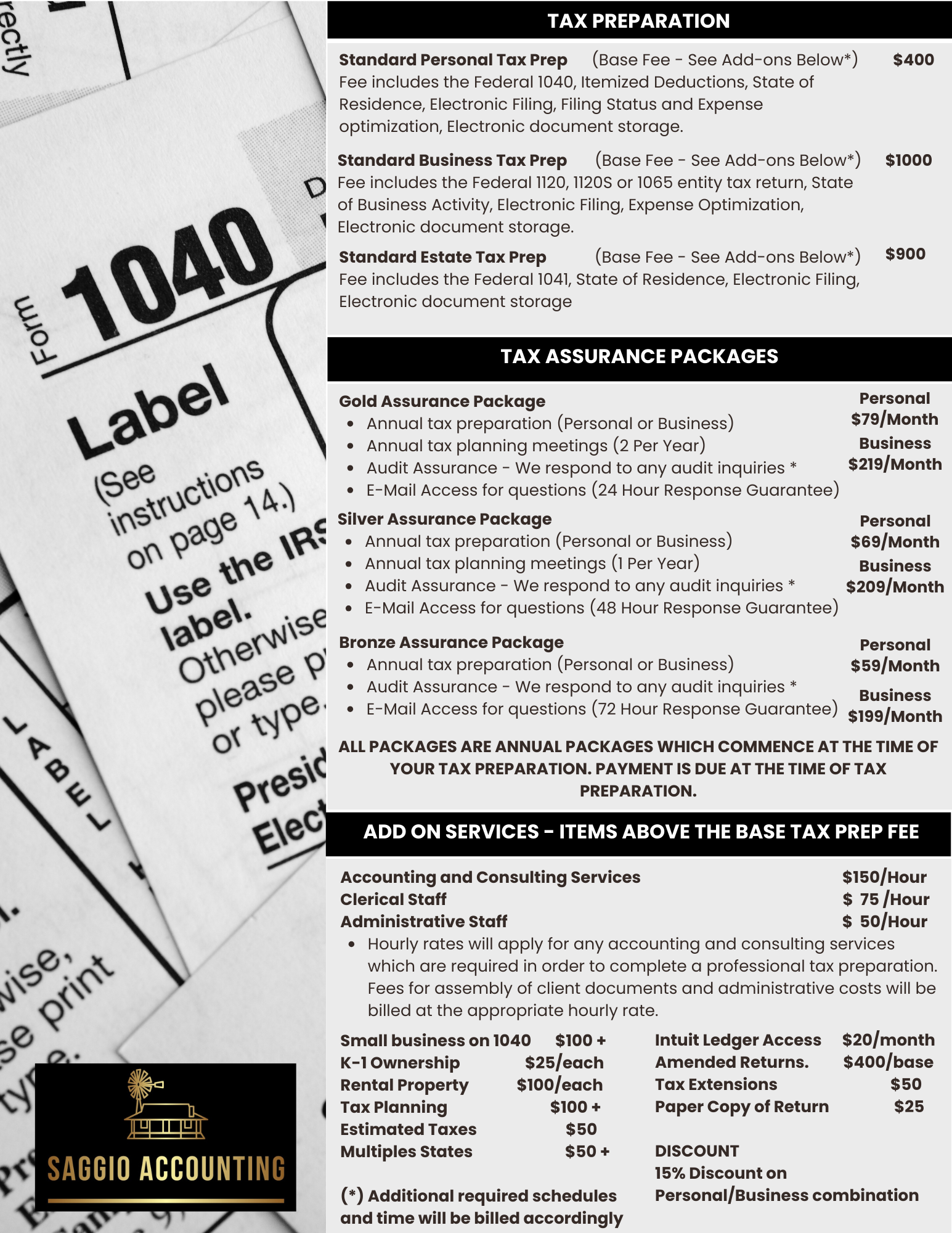

TAX ASSURANCE PRICING

Personal Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages.

Bronze Assurance Package

-

Annual Tax Preparation

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail Access for questions (36 Hour Response)

TAX ASSURANCE PRICING

Business Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages. These packages include both the business and personal tax related preparation services.

Bronze Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail access for questions (48 Hour Response)