Blog

We keep you up to date on the latest tax changes and news in the industry.

Understanding Tax Deductions for Scam Losses

Victims of scams often face not only emotional distress but also the complexity of navigating tax implications for restitution. While legislative shifts have historically narrowed the path for claiming deductions related to theft and casualty losses, strategic avenues remain open for victims, especially those engaged in profit-motivated activities.

Traditionally, tax laws permitted the deduction of theft losses when not covered by insurance. However, recent changes have tightened these rules, mainly limiting deductions to losses associated with federally declared disasters. Yet, important exceptions exist for those affected by scams linked to transaction activities intended for profit.

Internal Revenue Code Section 165(c)(2) provides relief specifically for losses incurred in profit-driven activities. If your scam losses were part of a legitimate profit-seeking venture, you might still qualify for a deduction, offering some fiscal recuperation for the ordeal endured.

Key Criteria for Profit-Driven Theft Loss Deductions: Certain stringent criteria must be fulfilled to leverage this deduction exception:

Profit Motive: Transactions must primarily aim at economic gain, necessitating explicit documentation to substantiate the intent for profit. IRS guidelines emphasize the necessity for bona fide profit expectations, requiring robust evidence such as investment documents or transaction records.

Transaction Type: Eligible transactions typically involve traditional investments like securities or real estate. Personal dealings or social activities are generally inadmissible for these kinds of deductions.

Source of Loss: The loss must directly correlate to a profit-seeking transaction, demonstrable through financial and legal records. Investment frauds or fraudulent schemes aimed at enticing investments often meet these requirements.

IRS Guidance Application: Implementing this deduction mandates a thorough review of IRS memoranda and related rulings to confirm loss eligibility. One noteworthy example pertains to IRS Chief Counsel guidance, highlighting deductible scenarios under qualifying circumstances.

Investment Scams: Even in cases of deceit, losses from credible profit-oriented investments may qualify for deductions, provided adequate proof substantiates the transaction's legitimacy and profit intent.

Theft Losses: Scrutiny is intense for profits-driven theft deductions, demanding proof that the loss ensued from a transaction initiated for financial gain rather than personal misfortune.

Conversely, unfavorable tax ramifications emerge when scams extract from IRAs or tax-deferred savings. Premature distributions due to scams often incur taxable income recognition and can usher individuals into higher tax brackets, compounded by potential early withdrawal penalties.

The implications starkly differ between traditional and Roth accounts. Traditional IRA withdrawals are tax-heavy, potentially increasing liabilities or incurring penalties if withdrawn prematurely. Meanwhile, Roth IRA withdrawals, assuming compliance with the five-year rule, are less burdensome but carry risks if non-qualified earnings are involved.

The following examples highlight essential scenarios distinguishing qualifying from non-qualifying losses and underlying tax repercussions. Often, these cases involve funds transferred abroad, with negligible retrieval prospects — a qualifying aspect for personal casualty loss.

Example 1: Impersonator Scam - Qualifies for Personal Casualty Loss

In this scenario, a taxpayer is deceived by an impersonator claiming to secure finances through new investment channels. The taxpayer's actions, underlined by reinvestment intent, endorse loss eligibility based on pursuit for economic advantage.

Tax Impact:

- If itemizing, a schedule deduction is possible.

- Taxable income must include traditional IRA distributions, and gains or losses on non-IRA funds must be recognized. Additionally, underage withdrawal penalties may apply.

- Resources permitting, re-rolling the funds into an IRA within 60 days averts tax consequences.

Example 2: Romance Scam - Does Not Qualify for Personal Casualty Loss

This example illustrates a taxpayer's financial commitment, misdirected by personal motivations devoid of any profit-seeking purpose. IRS regulations disallow losses lacking financial investment orientation under non-disaster casualty provisions.

Such circumstances can't leverage deductions despite taxation and potential penalties from IRA distributions.

Example 3: Kidnapping Scam - Does Not Qualify for Personal Casualty Loss

This scenario depicts distress-driven financial transfers devoid of profit intent and thus fails the deduction eligibility checks. Despite fraudulence, absence of an investment motive renders the losses non-deductible.

These illustrative cases underscore the necessity to consider not only the transaction's structure but also the involved financial intent. Documentation proving profit-directed intent not only aids in potential recovery but aligns with IRS scrutiny expectations.

It is imperative to seek consultations with our office pre-transfer when suspecting dubious communications. Our expertise offers significant value in fraud detection and preemptive measures. Educating family members, particularly vulnerable seniors, can mitigate risks, reinforcing our collective safeguarding mission.

Consult Saggio Management Group Inc. for personalized guidance on navigating these nuanced tax implications with integrity and clarity.

Sign up for our newsletter.

Each month, we will send you a roundup of our latest blog content covering the tax and accounting tips & insights you need to know.

We care about the protection of your data.

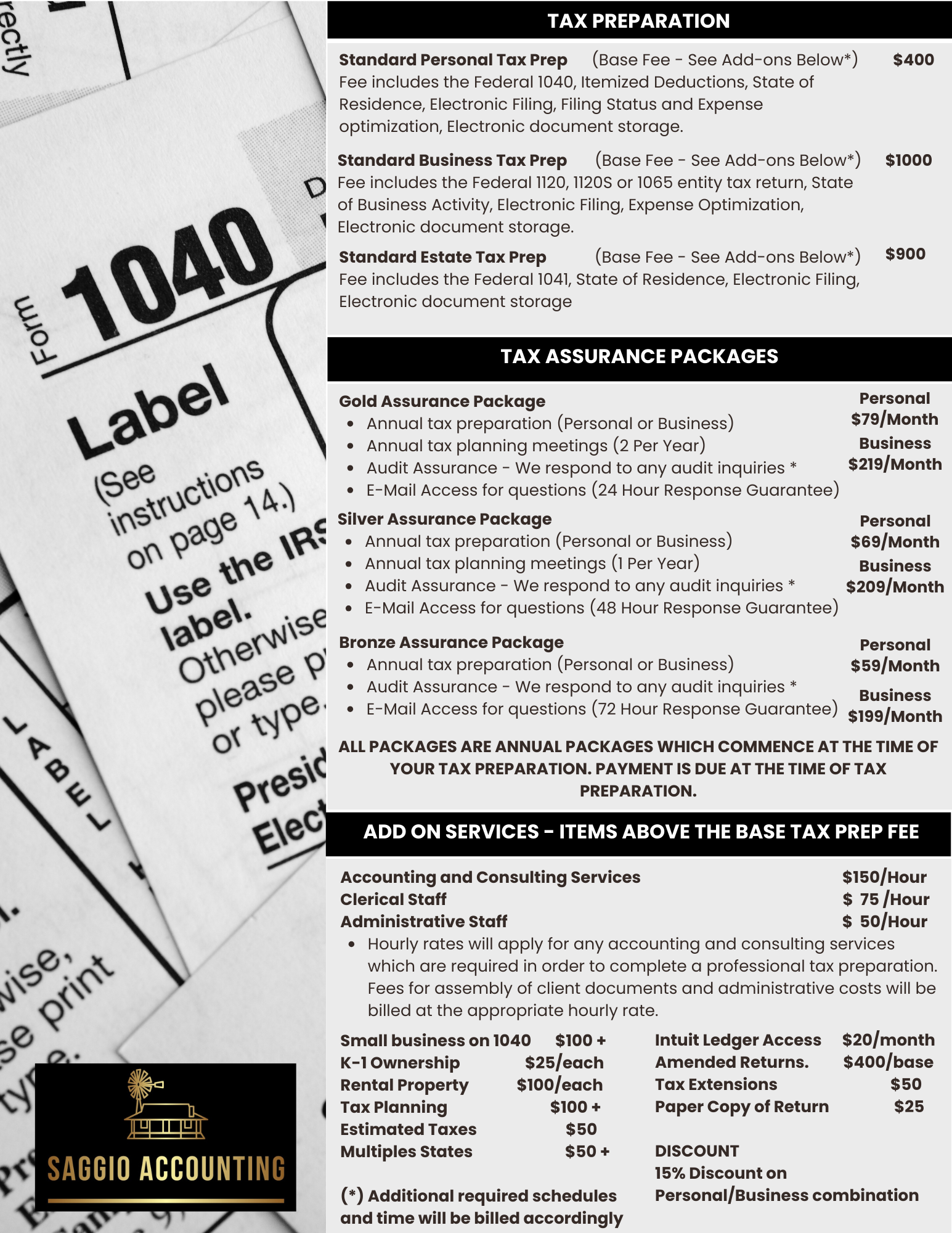

TAX ASSURANCE PRICING

Personal Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages.

Bronze Assurance Package

-

Annual Tax Preparation

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail Access for questions (36 Hour Response)

TAX ASSURANCE PRICING

Business Income Tax Services

In addition to our normal tax preparation service, we also offer the Tax Assurance Packages for those clients who want more than just a tax preparation. These packages are annual packages which provide superior tax preparation, tax planning and access to a tax expert via e-mail. All of these additional services are free of charge to those clients who select on of our Tax Assurance Packages. These packages include both the business and personal tax related preparation services.

Bronze Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (72 Hour Response)

Gold Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

2 Tax Planning Meetings per year

-

Audit Assistance - We respond to audit inquiries

-

E-Mail Access for questions (24 Hour Response)

Silver Assurance Package

-

Annual Tax Preparation (Business and Personal)

-

Annual Tax Planning Meeting

-

Audit Assistance - We respond to audit inquiries and E-Mail access for questions (48 Hour Response)